Issue No. 12

Where to Find Us

Esoteric Asset Finance | NYC | June 10, 2024

FinovateFall 2024 | NYC | September 9-11, 2024

US Asset Based Finance | NYC | Sept 30, 2024

Fintech Specialty Finance Forum | Laguna Niguel | December 4-6, 2024

iConnections Global Alts 2025 | Miami | January 27-30, 2025

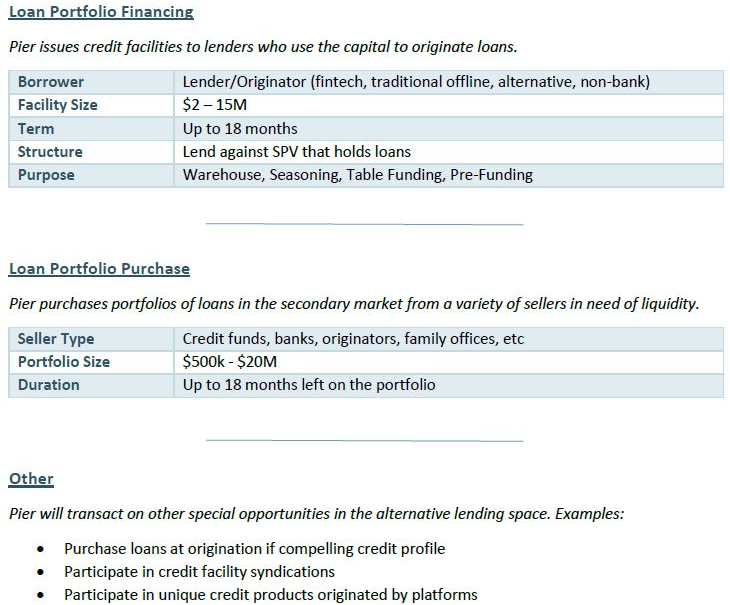

A Friendly Reminder

For this month’s newsletter I’m excited to remind our broader community the type of transactions we fund here at Pier. See below for details. We appreciate any and all deal referrals!

- Jillian

A note from the CIO- Credit Cards

Cassandra Doeng on our investment team recently read Four Winds by Kristin Hannah and offers this review: On the canvas of the Great Depression and the Dust Bowl, as an imperfect model with indomitable strength, Elsa Martinelli paints a picture of making the best out of the impossible for her two young children and herself. From Texas to California, their journey continues across the landscapes of suffering and survival. It took too many years, yet it's never too late, for Elsa to love, and to have a voice, through the timeless struggle with the shimmering whispers of hope.

Stay in the know

from Pier Asset Management straight to your inbox.

FINANCIAL DISCLOSURE

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Integer vitae imperdiet purus. Sed eget purus mollis, imperdiet sem ullamcorper, elementum justo. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Integer cursus nisl lectus, eleifend dictum ipsum placerat at. Fusce luctus fermentum ipsum, a sagittis neque rutrum at. Pellentesque eleifend libero non ante pellentesque, auctor mattis felis accumsan. Morbi sagittis eu felis eu varius. Donec interdum congue erat. Orci varius natoque penatibus et magnis dis parturient montes, nascetur ridiculus mus. Vestibulum bibendum risus id nunc luctus blandit. Aenean tincidunt urna quis turpis sodales placerat.