Issue No. 19

Where to Find Us

iConnections Global Alts | Miami | January 27-30, 2025

RMAI Annual Conference | Las Vegas | February 10 - 13, 2025

SF Vegas | Las Vegas | February 23 - 26, 2025

Fintech Meetup | Las Vegas | March 10 - 13, 2025

Music Biz | Atlanta | May 12 - 15, 2025

The Right Key Persons

Chart-watch

The charts we are looking at to understand the world around us

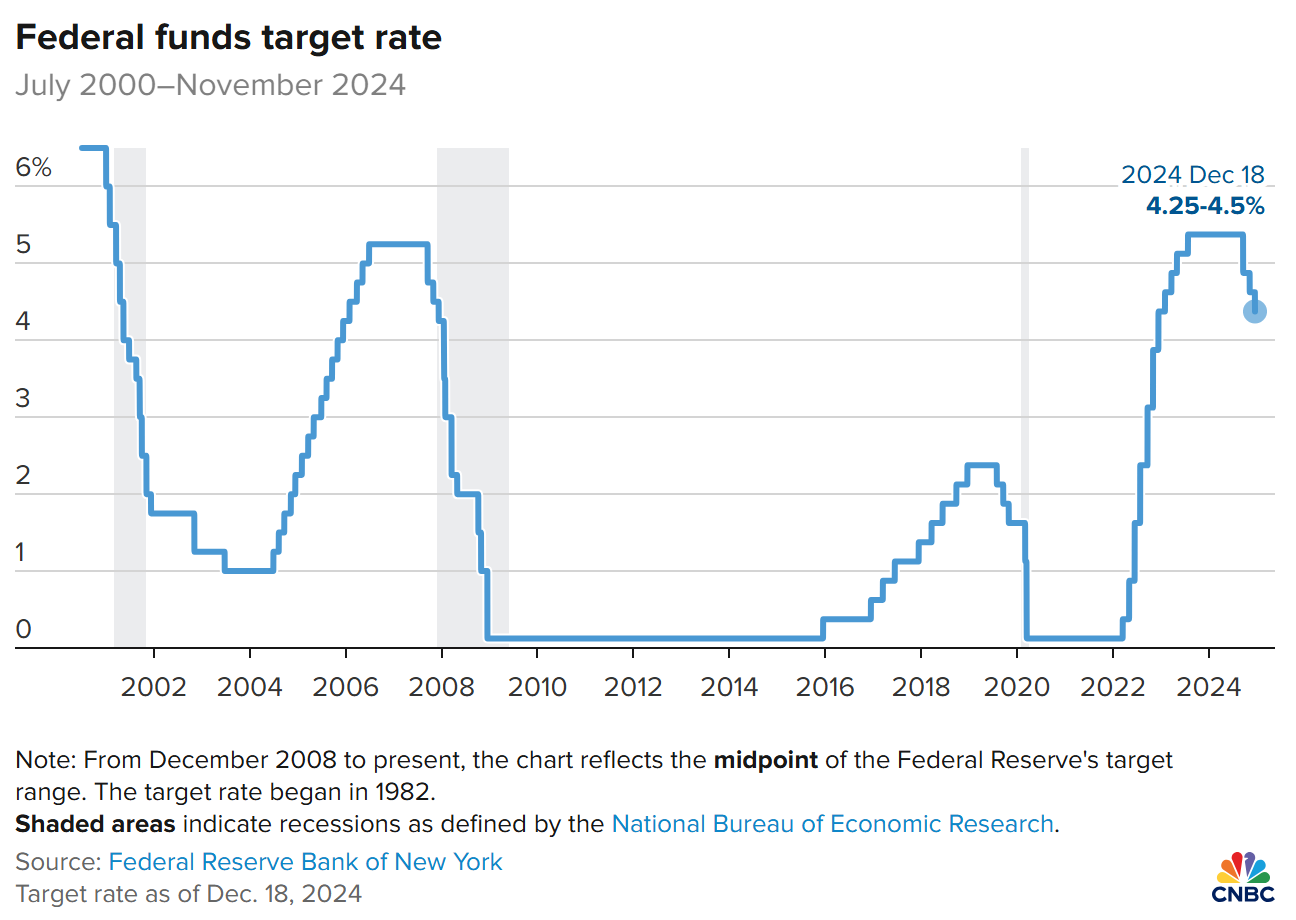

I've seen several economist predictions with the average being ~3.75% expected by the end of 2025.

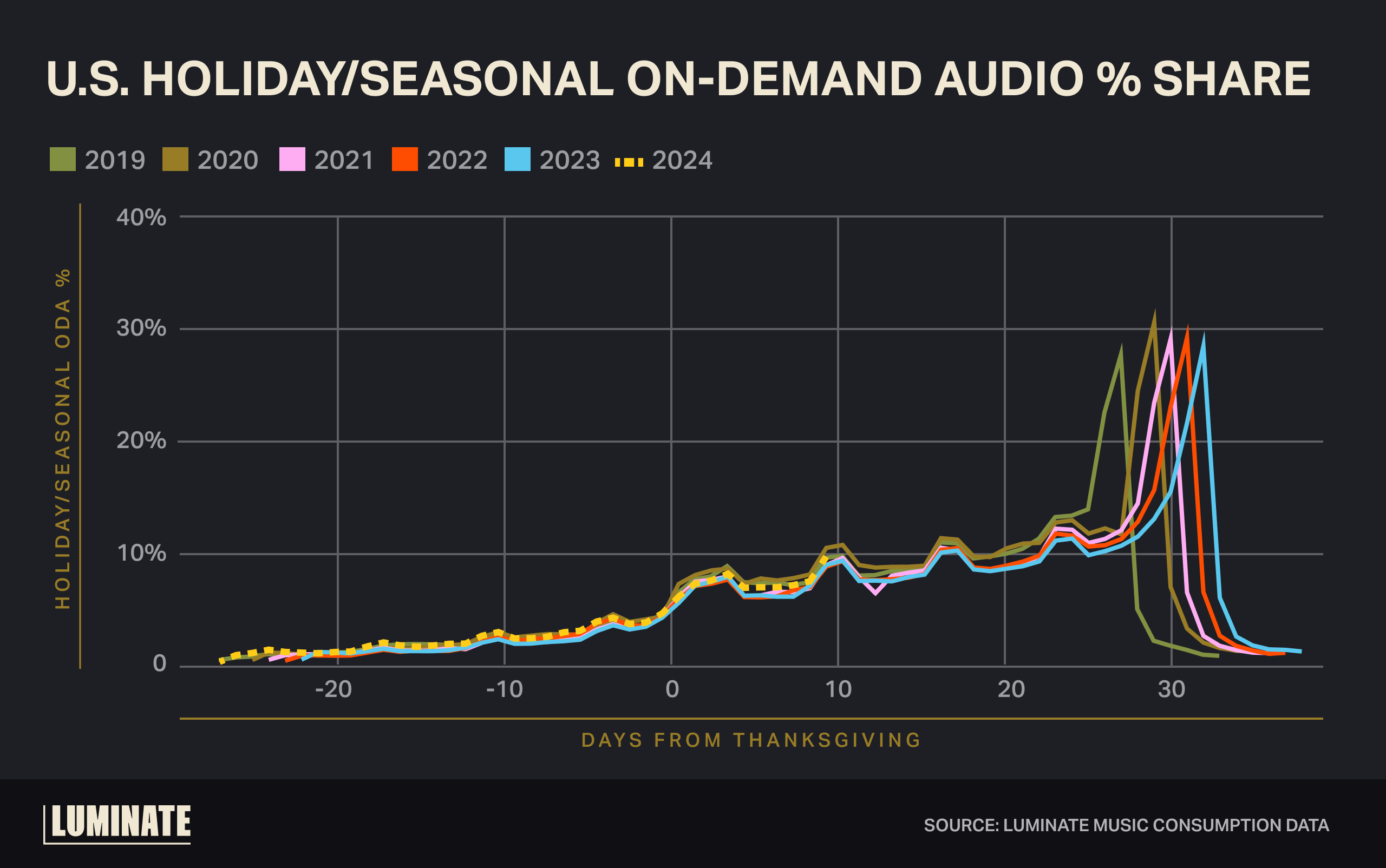

'Tis the season to listen to holiday music. While an annual anomaly, the stability of holiday music listening each year, starting around Thanksgiving, is fascinating to track.

A note from the CIO: The anatomy of a secondary loan portfolio purchase

Here is a deal you all may find interesting. In December, Pier purchased a portfolio of $21.7MM of subprime auto loans for 57.7% of par (~$12.5MM). Using conservative default rate and recovery expectations in our DCF model, we priced this using a 20% discount rate. How did we get there?

First, some portfolio stats:

- Loans: 1,797

- Avg Balance: $12,545

- Avg Orig Bal: $17,470

- Avg Duration: 10 months

- Avg Term: 48 mo

- Avg Seasoning: 14 mo

- Avg APR: 23%

- Approximately 6.9% of the portfolio is greater than 30 days past due.

- The collateral consists of standard car makes and models: Chevy, Ford, Kia, Nissan, Dodge, etc., with an average model year of 2014 and ~115k miles.

Seller: The seller was a buy here pay here originator in the Midwest, whose desire was to pay of their lender due to the difficult origination limitations set on it and other onerous terms, such as personal guarantees. The seller services their loan portfolio and maintains close relationships with their customers, frequently handling maintenance or refinancing into new vehicles.

The seller has been in business for 35 years and we received performance history going back almost two decades. The seller will retain servicing, which means the borrowers will see no change in their day to day loan situation.

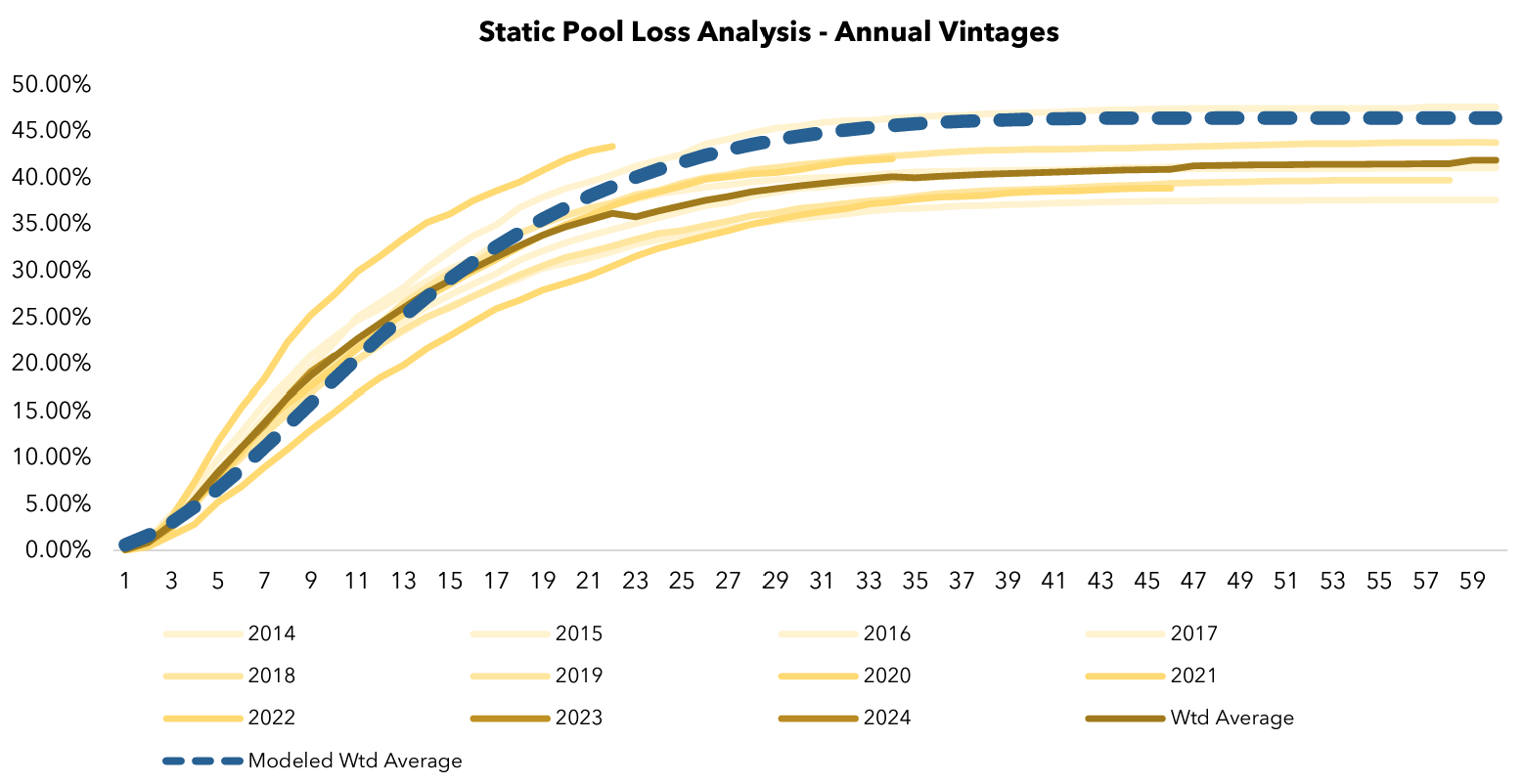

Performance: Cumulative loss curves the last decade have ranged from approximately 35% to 45%, averaging about 40% with 2022 as an outlier that is trending toward 47%. Approximately 15.6% of our portfolio was from 2022.

Recovery rates have varied historically, but they have been as low as 15% recently with this originator. Industry recovery rates have coming down, though 15% is at the low end of what we typically see in auto, especially since unsecured consumer defaults can generate as much as 8-12% in a bad debt sale.

Pricing: Given this information, we used cumulative default curves that average about 46%, and recovery expectations at 15%. We feel both of these numbers are conservative. Then, the cash flows from each modeled loan were discounted at 20%. Delinquent loans are marked down significantly based on our separate delinquency markdown curve. All of this resulted in that 57.7% bid and purchase price.

Diligence: Upon acceptance of the bid, we proceeded with a 3-week diligence process. We hired a third party subprime auto firm who we have worked with prior and know to be extremely thorough. We also conducted on site diligence and a compliance/regulatory review. The sellers proved to be very professional, which is not always the case in this asset class.

Co-invest: Finally, we syndicated out 25% of the deal to a few of our LPs with our main fund holding the bulk of it.

Projections: In the end, we believe a 20% gross IRR over a 10-month average duration to be very realistic, with potential for it to come in at 22-23% if defaults stay low or recoveries are a bit higher than modeled. The monthly performance will have some real volatility to it as these types of portfolios do, but with diversification through this amount of volume, we don't expect performance straying due to small sample size. In a downside stress case we model a 9% gross IRR.

- Conor

P-WERM

Here are a bunch of 2025 outlooks that you should not listen to:

Vanguard - Beyond the landing Link

Robeco - 5-Year Expected Returns: Atlas Lifted Link

KKR - 2025 Outlook: Glass Still Half Full Link

Cambridge Associates - 2025 Outlook Link

JP Morgan - Out of the Cyclical Storm and into the Policy Fog Link

Goldman Sachs - Macro Outlook: Tailwinds (Probably) Trump Tariffs Link

Goldman Sachs - Global Equity Outlook: The Year of the Alpha Bet Link

Richard Bernstein Advisors - Certainties for an uncertain world Link

Charles Schwab - 2025 U.S. Stocks and Economy Outlook Link

UBS - The CEO Macro Briefing Book: 12 Questions Ahead of 2025 Link

Apollo - 2025 Economic Outlook: Firing on All Cylinders Link

Stay in the know

from Pier Asset Management straight to your inbox.

FINANCIAL DISCLOSURE

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Integer vitae imperdiet purus. Sed eget purus mollis, imperdiet sem ullamcorper, elementum justo. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Integer cursus nisl lectus, eleifend dictum ipsum placerat at. Fusce luctus fermentum ipsum, a sagittis neque rutrum at. Pellentesque eleifend libero non ante pellentesque, auctor mattis felis accumsan. Morbi sagittis eu felis eu varius. Donec interdum congue erat. Orci varius natoque penatibus et magnis dis parturient montes, nascetur ridiculus mus. Vestibulum bibendum risus id nunc luctus blandit. Aenean tincidunt urna quis turpis sodales placerat.