Issue No. 26

Where to Find Us

U.S. Asset Based Finance | New York | September 25 - 26

NAIC Amplifying Alts Forum| Los Angeles| October1-12

Money 20/20 | Las Vegas | October 26 - 29

Fintech Specialty Finance Forum | Dana Point | December 9 - 11

Why We Pass on Deals

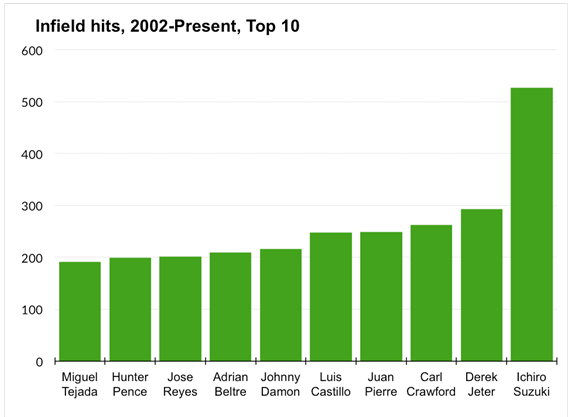

A note from the CIO: Home Runs Win Games, Small Ball Wins Championships

InFintech, the attention goes tothe 30% IRR deal, the hockey stick deck, orthe customer acquisition moat. But consistent wins come from getting on base,not swinging out of your shoes.

We love singles. Loan portfolios where the data’s clean. Borrowers who havegrown origination volume 15% year on year, not week on week. We do not aim forterms that areheroic...just durable. We do deal after deal, month aftermonth, with a focus on senior secured debt over-collateralized by financial assets.

That doesn’t mean we don’t make errors. We haveseen originators with asolid team and product stumble on early vintages. We have bought loanportfolios that underperformed after a servicing change.

But when your strategy is built around getting on base, you can afford anerror. What you can’t afford is swinging for the fences every time and strikingout with the bases loaded. So don’t try to be Cal Raleigh. Be Ichiro Suzuki.Get on base. Extend the inning. Rack up hits slowly and surely, and the realwinners are still playing in October.

– Conor

MCRR - Minimum Cumulative Collections Rate measures the lowest acceptable percentage of expected cash collections (such as loan repayments, leases, or receivables) that must be received over a defined period. We avoid excessive acronyms here at Pier, but "MCRR" entered our official lexicon last month.

Whyare we thoughtful about which acronyms are "officially"adopted? Elon Musk has a good take in his now famous email from 2010, Acronyms Seriously Suck

Stay in the know

from Pier Asset Management straight to your inbox.

FINANCIAL DISCLOSURE

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Integer vitae imperdiet purus. Sed eget purus mollis, imperdiet sem ullamcorper, elementum justo. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Integer cursus nisl lectus, eleifend dictum ipsum placerat at. Fusce luctus fermentum ipsum, a sagittis neque rutrum at. Pellentesque eleifend libero non ante pellentesque, auctor mattis felis accumsan. Morbi sagittis eu felis eu varius. Donec interdum congue erat. Orci varius natoque penatibus et magnis dis parturient montes, nascetur ridiculus mus. Vestibulum bibendum risus id nunc luctus blandit. Aenean tincidunt urna quis turpis sodales placerat.