Issue No. 3

Where to Find Us

Specialty Lender Finance US (NYC) | Sep 18, 2023

Money 20/20 (Vegas) | Oct 22-25, 2023

Opal Lending Summit (Dana Point) | Dec 5-6, 2023

iConnections (Miami Beach) | Jan 29-Feb 1, 2024

Fintech Meetup (Las Vegas) | March 3-6, 2024

International Factoring Association (Miami Beach) | May 1-3, 2024

Smart Creatives

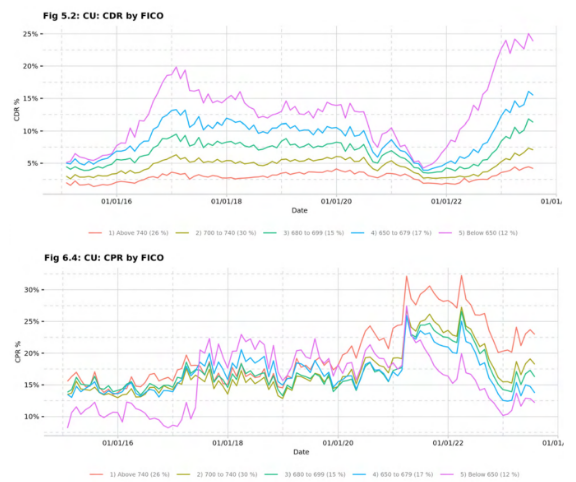

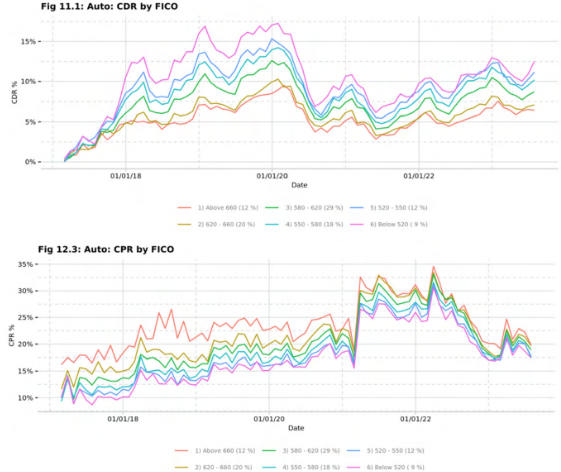

A note from the CIO - Runoff Models

Conor and Jonathan recently finished a fantastic feel good book: A Gentleman in Moscow, by Amor Towles. The lively, elegant, and almost silly novel serves as a great reminder of the value of doing the right thing.

Stay in the know

from Pier Asset Management straight to your inbox.

FINANCIAL DISCLOSURE

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Integer vitae imperdiet purus. Sed eget purus mollis, imperdiet sem ullamcorper, elementum justo. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Integer cursus nisl lectus, eleifend dictum ipsum placerat at. Fusce luctus fermentum ipsum, a sagittis neque rutrum at. Pellentesque eleifend libero non ante pellentesque, auctor mattis felis accumsan. Morbi sagittis eu felis eu varius. Donec interdum congue erat. Orci varius natoque penatibus et magnis dis parturient montes, nascetur ridiculus mus. Vestibulum bibendum risus id nunc luctus blandit. Aenean tincidunt urna quis turpis sodales placerat.